IDC’s latest Worldwide Semiannual Security Spending Guide

According to IDC’s latest Worldwide Semiannual Security Spending Guide, spending on security hardware, services, and software in Asia/Pacific excluding Japan (APeJ) is expected to reach $36 billion in 2024, an increase of 12.3% over the previous year.

With the evolving threat landscape and increasing complexities, organizations in the region are prioritizing investments in security-related products and services, recognizing their critical importance in safeguarding against emerging risks.

IDC expects spending on security to grow at a five-year CAGR of 12.8% over the forecast period (2022-27) and reach USD 52 billion by 2027.

“The surge in cyber threats utilizing AI, such as deepfakes, pretexting, and identity theft, has spurred a heightened demand for comprehensive security solutions in the region that encompass threat detection, automated remediation, and behavioral analysis capabilities,” says Sharad Kotagi, Market Analyst, IT Spending Guides, IDC Asia/Pacific.

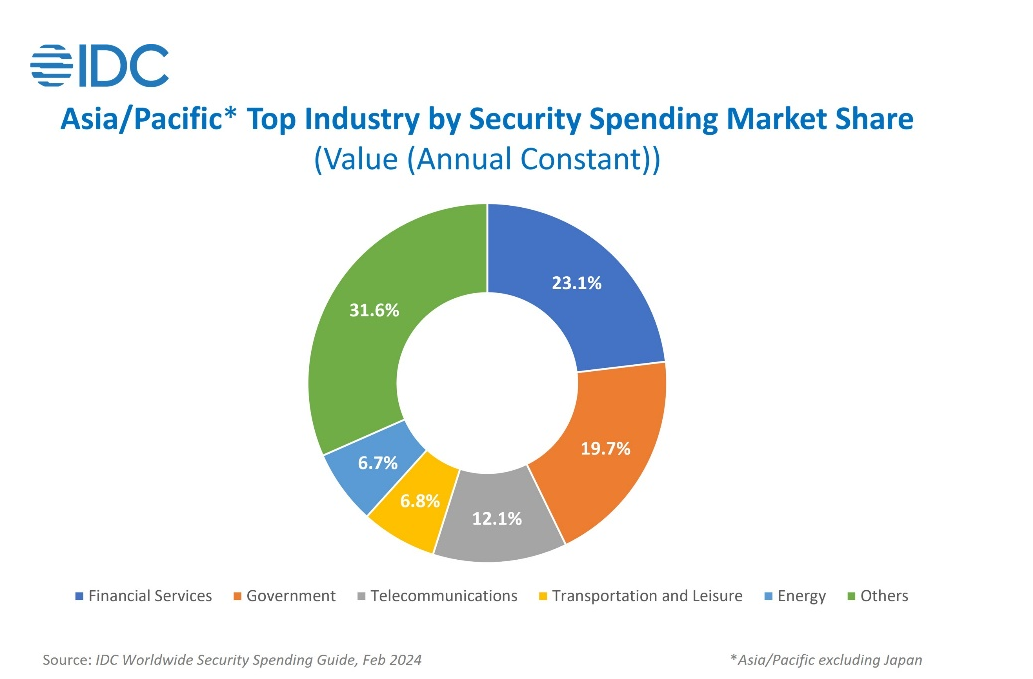

In 2024, the Financial Services, Government, and Telecommunications sectors remain the leading investors in security solutions from an industry end-user perspective.

Together, these industries contribute to over 50% of the total security spending in APeJ. Industries are investing strategically to keep up with technological advancements such as open banking, digital payments, e-governance, modernization of IT infrastructure, and changing compliance regulations.

Software and Information Services, and High Tech and Electronics are showing the fastest growth in 2024.

The demand for security in complex IT environments, including networks, cloud services, and endpoints, is high, amid a cybersecurity talent shortage.

This creates opportunities for vendors and partners to provide varied security services. Services, especially Managed Services, will lead the market, forming nearly 40% of security spending, growing at a 12.8% five-year CAGR.

“Regulatory requirements and data protection laws will be a catalyst for spending on security consultation and integration services, while the managed security services market will be buoyed by the increasing complexity of IT environments and the persistent shortage of cybersecurity talent in the region,” says Benjamin Ten, Research Analyst, IT Services, IDC Asia/Pacific.

Cyberattacks are increasing in APeJ, necessitating a shift in addressing cyber threats. China leads regional security investments, comprising over 40% of total spending in 2024, with a 13.5% five-year CAGR. Australia and India are next, contributing over 25% to the APeJ security spending.

The Worldwide Security Spending Guide quantifies the global revenue opportunity for both core and next-generation security purchases with detailed forecast data for security spending by 28 industries across nine regions and 53 countries and 5 company size bands.

(Courtesy: www.IDC.com)